STIFEL: WRE ($32.06, Hold) - Maryland Athletes Win Twenty Olympic Medals While WRE Happy to Exit Maryland Office Market. NDR Recap. Hold

Maryland Athletes Win Twenty Olympic Medals While WRE Happy to Exit Maryland Office Market. NDR Recap. Hold. |

|

|

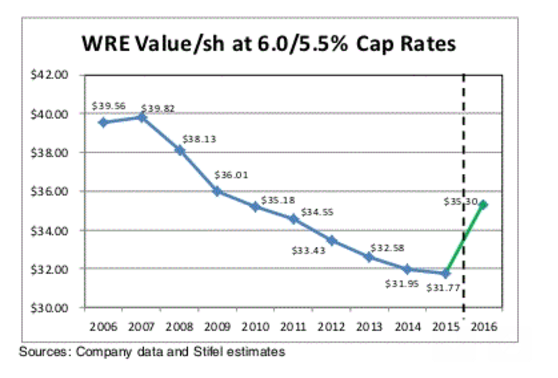

- This adjustment creates a one-time pop to NAV. Where the value goes hereafter will once again depend upon management's ability to create value in a still challenging Washington, D.C. environment. WRE's improved cost of capital, should help in this respect.

- It appears as if all REITs (all sectors) that are generating reasonable (5%+) FFO/FAD growth, can grow the dividend and own institutional quality assets are trading sub 5.3%. As WRE clearly owns institutional quality assets, share price appreciation appears likely if the portfolio starts generating earnings and dividend growth.

- We think the post suburban office portfolio sale TEV for office space of $455/SF is fair relative to our recently updated $592/$433/SF estimates for gross/adjusted replacement cost.

- Other positive aspects include 1) improved balance sheet, 2) improved portfolio, 3) while the Washington, D.C. economic recovery lagged the U.S. 2011-2015, it is now exceeding the U.S., 4) Washington, D.C. leads the nation in millennial as a percentage of the population, and 5) WRE has internal redevelopment opportunities for both office and apartment assets.

- Negatives include 1) there is not a shortage of talented developers in the Washington, D.C. MSA, 2) land is available near a large number of METRO stops, 3) significant apartment supply, 4) surprising continued office development in select markets.

- We are adjusting our 2016 FFO/FAD/sh estimates to $1.77/$1.28 from $1.77/$1.32 and our 2017 FFO/FAD/sh estimates to $1.81/$1.30 from $1.80/$1.29. This equates to normalized FFO/FAD 2015-2017 growth of 2.9%/2.8%.